Maryland statewide sales and use tax rate for most taxable retail sales.

Remote sellers should monitor Maryland gross sales against the economic nexus threshold.

Maryland also uses a separate transaction-count threshold for remote sellers.

Quick answer for ecommerce sellers.

If you sell taxable products or taxable services into Maryland, you may need to register, collect, file, and remit Maryland sales and use tax if you have Maryland physical presence or meet Maryland economic nexus rules. Maryland remote sellers generally monitor whether Maryland gross sales exceed $100,000 or whether they have 200 or more separate transactions in the current or previous calendar year.

Maryland is easier than many local-rate states because it generally uses one statewide sales tax rate. The work still requires clean source files: direct ecommerce sales, marketplace sales, exempt sales, refunds, tax collected, and filing confirmations.

What creates Maryland sales tax nexus?

Maryland nexus can come from physical presence, employees, inventory, representatives, or remote seller volume. A merchant should review fulfillment locations, marketplace channels, direct orders, and Maryland sales history before registration decisions.

- Physical presence: employees, property, inventory, contractors, or regular business activity in Maryland can create obligations.

- Economic nexus: monitor gross sales against $100,000 and transaction counts against 200.

- Marketplace activity: marketplace-facilitated sales should be separated from direct sales for review and filing.

- Taxability: most tangible personal property is taxable, while groceries, prescription drugs, medical items, and exempt/resale sales need support.

How Maryland registration fits into the workflow.

Maryland businesses commonly register and manage tax accounts through Comptroller of Maryland online services. Before registering, gather the legal entity name, EIN, responsible party, business address, sales start date, channel list, product categories, marketplace reports, and payment owner.

After the account is active, save the Maryland sales and use tax account details, online login owner, filing frequency, payment method, exemption process, and reviewer assignment in the compliance workspace.

Collection, taxability, and marketplace sales.

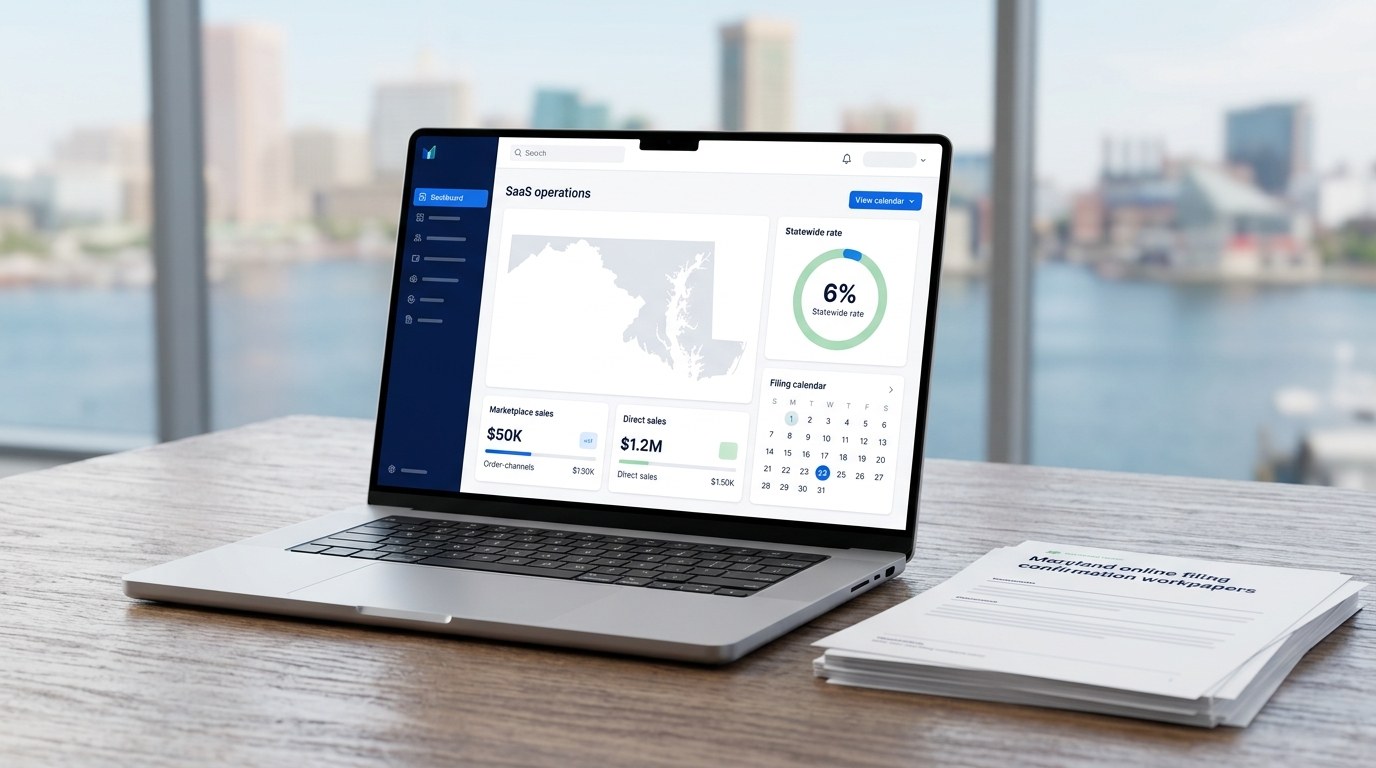

Maryland generally has a 6% statewide sales and use tax rate with no general local sales tax add-ons. Alcoholic beverages and some product categories can have different treatment, so product mapping still matters.

- Direct ecommerce sales: orders where the merchant is seller of record and may need to collect Maryland tax.

- Marketplace sales: Amazon, Walmart, Etsy, eBay, and other marketplace orders should be isolated before filing prep.

- Exempt and resale sales: retain resale certificates and exemption documentation with the return packet.

- Refunds and adjustments: returns, credits, and tax adjustments should tie to the exact filing period.

How to prepare a Maryland sales tax filing packet.

Maryland sellers commonly file sales and use tax returns through the Comptroller's online tax services. Filing frequency depends on the account. Monthly and quarterly returns are commonly due by the 20th day after the reporting period, and annual returns commonly follow a January 20 deadline.

- Export exact-period reports: pull order, refund, tax, marketplace, exemption, and payout reports.

- Separate channels: split direct ecommerce orders from marketplace-facilitated sales.

- Map Maryland totals: document gross sales, taxable sales, exempt sales, deductions, and tax collected.

- Reconcile data: compare platform tax, payment processor data, accounting, and marketplace reports.

- Prepare reviewer notes: record source files, assumptions, exceptions, preparer, reviewer, and approval time.

- Save proof: keep the filing confirmation, payment receipt, source exports, and final workpapers together.

What happens if Maryland filings are late or unsupported?

Late filing, late payment, unsupported exemptions, marketplace duplication, missing source reports, and unreconciled refunds can create penalties, interest, notices, amended returns, or audit work. A simple statewide rate does not remove the need for complete records.

Before filing, review this checklist:

- Does the filing period match every source export?

- Are direct and marketplace sales separated?

- Are resale and exemption records saved?

- Do refunds and tax collected reconcile to accounting?

- Was the filing confirmation and payment proof saved?

Maryland sales tax FAQ.

What is Maryland economic nexus?

Maryland remote sellers generally monitor whether Maryland gross sales exceed $100,000 or whether they have 200 or more separate transactions in the current or previous calendar year.

What is the Maryland sales tax rate?

Maryland generally has a 6% statewide sales and use tax rate and no general local sales tax add-ons.

Where do Maryland sellers file?

Maryland sellers commonly file sales and use tax returns through the Comptroller of Maryland online tax services.

Do marketplace sales need to be separated?

Yes. Marketplace-facilitated sales should be separated from direct ecommerce sales because collection and reporting responsibility may differ.

Can AtomicTax help file Maryland returns?

Yes. AtomicTax helps ecommerce merchants prepare filing-ready packets and complete standard sales tax filings for $45 per filing.

Official Maryland resources to check.

Need help making Maryland filings repeatable?

AtomicTax prepares sales tax filing packets from ecommerce reports, separates marketplace and direct-channel activity, and helps merchants keep every filing period reviewable.